Members Directory

Important Note:

Leo Penney: Just spoke with an underwriter about a decline that made no sense on one of our cases. I thought it should have been 200%, which is what Manu would have rated except he had been declined within the past year by TD. I'm told Karen Cutler, their chief underwriter, just issued a directive that any case that has been declined by another carrier within the past year will now be declined by Manu during the covid19 epidemic.

Manulife

May 11th 2020: Anticipating delays: Operating in different times, adopting different expectations

April 27th 2020: Making it easier to submit segregated fund and GIC business during Coronavirus

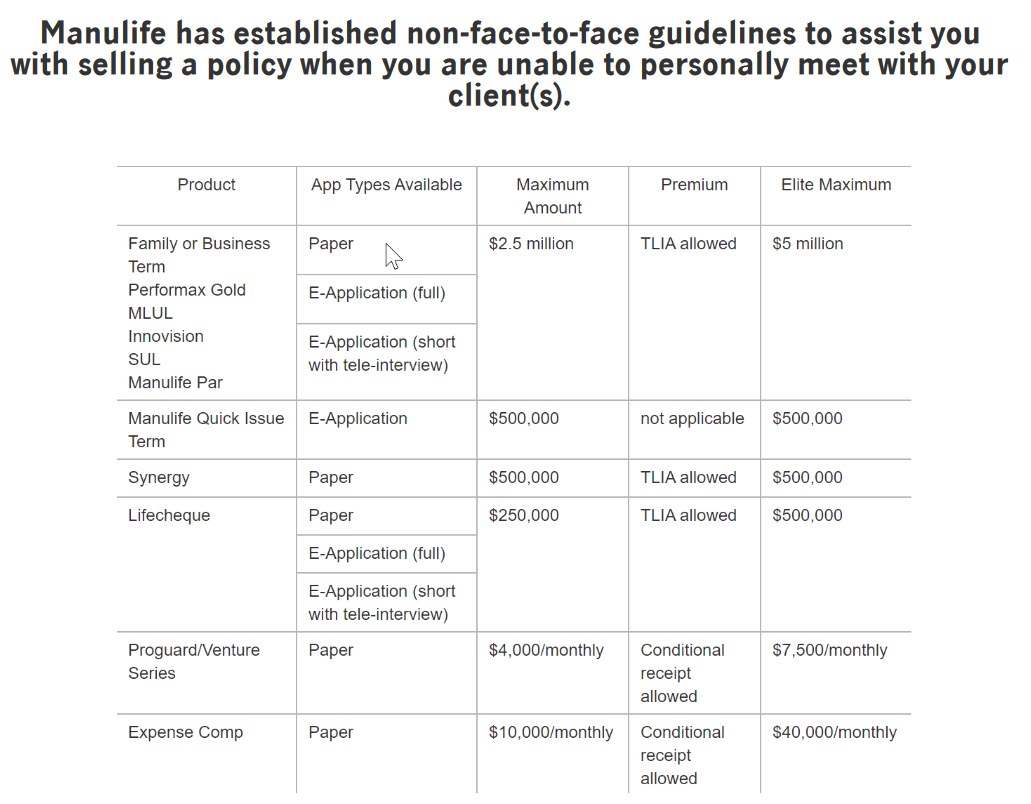

April 13th, 2020: Keeping insurance applications and contracts moving despite COVID-19

April 9th, 2020: Extending payment grace periods

We’re taking our industry leading testing limits to a new level on a temporary basis – your healthiest non-smoking clients can now get coverage without fluids for Term, UL and Par cases.

Ages 18-50 $2mm or less (previous limit $1mm)

Ages 51-60 $1mm or less (previous limit $100,000)

We estimate about 50-60% of applicant’s currently tested in the expanded ranges won’t need to be tested.

Healthstyle 3 rates will apply, HS 1 & 2 will not be available.

We will follow the established Accelerated program - we will request biometric testing for higher risk cases:

Examples of when we may request biometric tests include, but are not limited to, applicants who:

- Have a personal history of heart disease, stroke, cancer or diabetes.

- Have a significant family history of heart disease, stroke, cancer or diabetes

- Have three or more driving infractions within the last 24 months or have been charged with driving while impaired in the past 10 years.

- Have a build greater than our current Healthstyle 2 chart.

- Have been diagnosed with high blood pressure or elevated cholesterol prior to age 45.

- Fall under our “New Canadians Guidelines”.

If your client has been declined by another insurer in the last 12 months, don’t submit them for consideration under this temporary program.

We’ll be running our smoking algorithm on these cases, and some clients may require testing as a result of the analytics tool.

We will proactively review pending cases to see if we can waive the fluid testing that has already been requested.

Underwriters will be following these rules starting April 8, 2020.

- Please use electronic solutions and take advantage of self-serve resources available on Repsource, such as New Business Notifications (NBN), My Clients, and our Training Corner. See additional tips here.

- We remain focused on meeting our customers’ needs and will review each case to prioritize essential and critical work. There will not be any special handling, urgent requests or priority service during this time. We’ve also temporarily suspended preferential treatment for Elite inquiries until further notice.

- Due to the strain on the medical community at this time, we may not receive timely updates on doctor’s reports and other medical testing. Dynacare has suspended paramedical services and medical testing will generally not be available for new business. While Exam One and other vendors may be offering face to face paramedical services, Manulife has advised them that we’re temporarily discontinuing this service so that we can effectively support social distancing as requested by the Canadian and Provincial governments. We are reviewing our age and amount guidelines to provide temporary changes to testing limits. We will look at our pending business to determine if pre-arranged requirements as part of routine testing can be waived.

Covid-19 Resources -- Infosource (March 26th, 2020)

Updates to Manulife underwriting and new business during the Coronavirus (COVID-19) (March 24th, 2020)

Please click this link for a full update in the e-business handbook.

COVID-19: To stay current on this challenging and ever-developing situation, click here

How to keep your business moving during this time, click here